On top of people’s health, the U.S. economy is also taking a big hit. Consumers are dealing with everything from loans and refinancing to bankruptcy and unemployment, and that’s just the tip of the iceberg. Another group being affected are those investing in some kind of retirement fund. Whether they’re planning on retiring within the next year or they’re early on in their career and are proactively saving for their future, some consumers have changed their investing behavior due to the impact of COVID-19.

Who is increasing their retirement investment during this time? Who is decreasing their investment? It’s essential for banks to understand their account holders’ sentiment surrounding COVID-19 on a deep and dynamic level, so they can adjust their messaging, offers,communication and engagement strategy in a resonant, yet authentic way.

To access the insights available on retirement investments, we’re utilizing Connected Flash Studies. These studies are surveying real-time consumer sentiment across industries in the wake of the coronavirus pandemic. They are scaled to the entire U.S. adult online population of 200 million and can be integrated into your marketing ecosystem for immediate action. The screenshots you’ll see below are taken directly from our easy-to-use Ignite Platform.

Consumers Increasing Their Retirement Investment

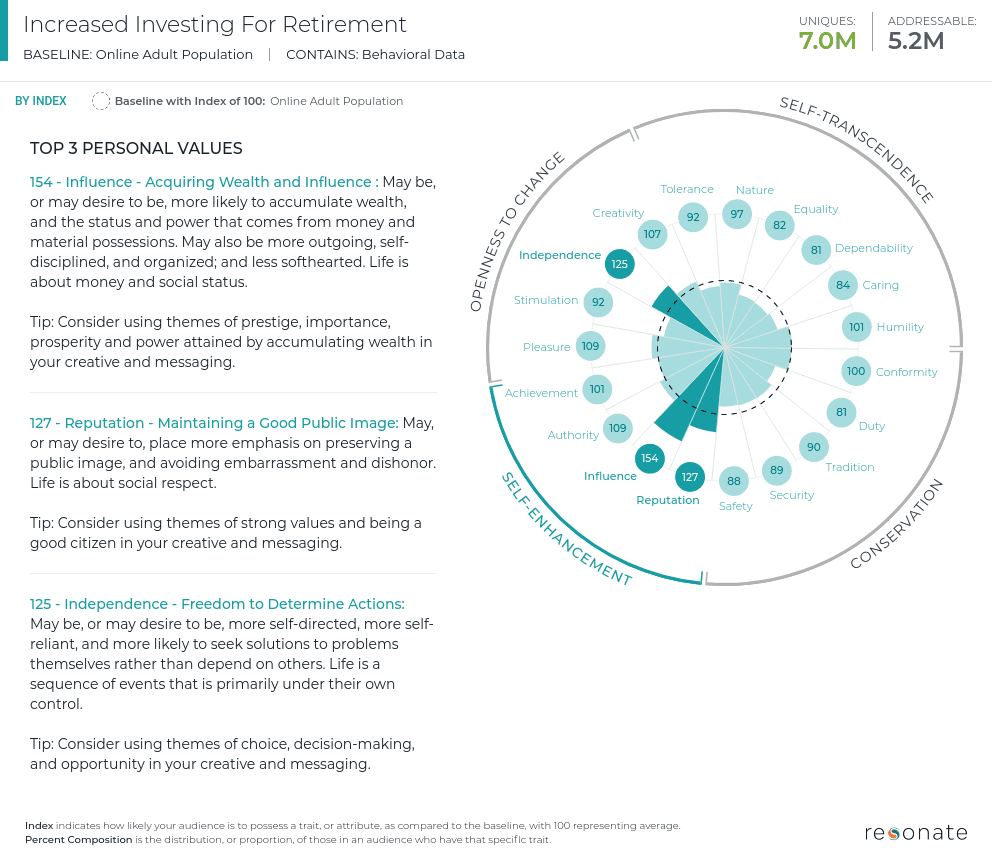

This group is mostly made up of married men ages 25-34 with no kids and a full-time job and an annual household income between $25-50K. When it comes to their top personal values, they over index for acquiring wealth and influence, maintaining a good public image and freedom to determine their own actions. This group likes to be in control and puts emphasis on increasing wealth, so it makes sense that in a time of so much uncertainty, this group, despite being decades away from retirement, is making decisions for their financial future.

What are their investment firm preferences and behaviors?

This group is 16% more likely to switch investment firms within the next 4-12 months. So, how do you ensure that your account holders aren’t one of these consumers thinking of switching to another firm?

This segment is 67% more likely than the average U.S. consumer to have a retirement account sponsored by their employer. The top firms they use are Fidelity, Vanguard and E*Trade. This group is 60% more likely to have an IRA, and their top firms are TD Ameritrade, Vanguard and Fidelity. Not surprisingly, they’re 99% more likely to try robo investing than the average U.S. consumer and 29% are persuadable on the idea.

Customers with non-employer-sponsored retirement accounts have less than $10K in their retirement fund, while those with an employer-sponsored account have between $10K-50K. Due to this group’s age, these lower numbers aren’t surprising, and it explains why this group may want to increase their savings during this turbulent time.

When it comes to choosing an investment advisor, this group is 56% more likely to prefer someone who has comprehensive stock trading tools, 35% more likely to prefer someone who has low fees on stock trades and 33% more likely to prefer someone with helpful online planning and reporting tools. Make sure your customers are fully aware of these offerings. Keep them informed of any new tools you’re adding and teasing ones you’ll be adding in the future will keep them invested (no pun intended).

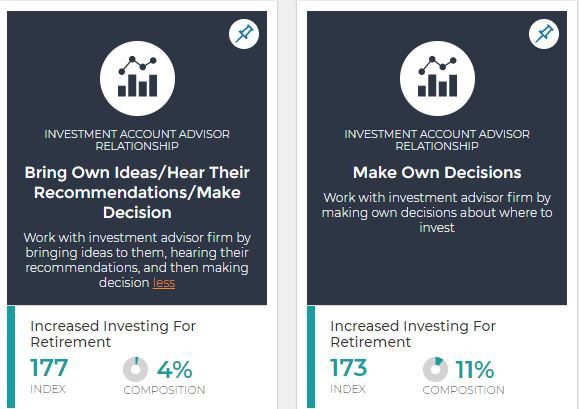

When it comes to their relationship with their investment account advisor, they’re 77% more likely to bring their own ideas, hear an advisor’s recommendations and, ultimately, make their own decision. They’re also 73% more likely to simply make their own decisions without input about where to invest, which ties into this group’s core value of determining their own actions. Since this group is all about making their own decisions, approach this group as a springboard to bounce ideas off, rather than telling them what to do when it comes to their investments. They pride themselves on their decision-making abilities, so keep them satisfied by letting them take the reigns on their account.

What Does This Mean for Investment Firms During the COVID-19 Crisis?

Based on what we’ve discovered about this audience in the Ignite Platform, this group skews younger and is attempting to plan for their financial future throughout the uncertainty surrounding the economy and job stability.

This group is focused on increasing their wealth and making their own decisions, so investment advisors should provide recommendations that help them achieve their financial goals, but not tell them explicitly what to do. They also value the available tools an advisor can offer, so keep them from jumping ship by teasing the launch of a new tool that’s coming soon and keep them informed of updates to current planning and stock trading tools.

Want to learn more about consumers during the COVID-19 crisis? Download our just released report: Understanding U.S. Consumer Sentiment During the Coronavirus Pandemic.