Buy now, pay later options, like Affirm, Klarna, and Afterpay, are winning the wallets of younger consumers, not yet making the money they need for high-dollar purchases, but not willing to swipe a credit card. These platforms are often advertised at checkout on a retailer’s website and allow users the option to split the cost of the item into several interest-fee payments over the course of six months or a year. These payments are directly debited from a bank account, so remembering to make a minimum payment isn’t necessary.

Get to know another retail audience and gain insights you need to connect. Download the Back-to-School Guide: The ABCs of Growing Revenue today.

Why Use a Buy Now, Pay Later Option?

For many buy now, pay later users, the option is appealing because it comes without the traditional interest rate of a credit card or the hit to their credit. They are limited in the amount that they can put on a particular platform, and, because it is automatically linked to their bank account, there’s no worry that they’ll forget a payment (good news since this group is 2X more likely than the average consumer to incur late or skipped payment fees on their primary credit card). However, for retailers, because these agreements are handled through a third party, there is less concern of risk.

If you’re looking to connect with consumers interested in buy now, pay later options, here are five quick insights that can help you reach them at the right time, on the right platform, with the right message.

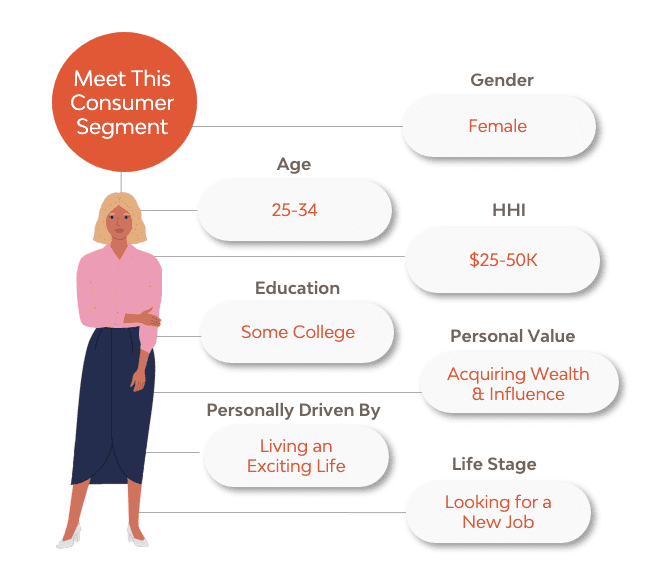

Meet the Buy Now, Pay Later Consumer

The buy now, pay later (BNPL) consumer is more likely to be a Gen Z or Millennial female. She’s early in her career, making a household income of $25-50K. There could be an element of “keeping up with the Joneses” that’s driving her to purchase items that are beyond her reach, but in a way that feels more attainable. If she buys a $200 dress, it’s going to hurt her wallet less on that first day if she only pays $50 — and then $50 again, three more times.

Insight One: They Value Acquiring Wealth and Influence

This BNPL consumer wants to project an air of “I’ve made it!”, even if she hasn’t yet — think of this as your upwardly mobile consumer. She may want the status symbol bag, the latest technology, and all the trappings of someone who’s already found success. She’s not willing to wait for it, but she’d also rather not go into credit card debt. Instead, she’ll shop at the retailers that signify wealth and influence in her circles, but she’ll make a purchase or two at a time and pay them off over the course of installments.

Source: Resonate Ignite Platform™, August 2021

Insight Two: They’re Looking for a New Job

While looking for a new job, the upwardly mobile BNPL consumer will need the laptop, the leather tote, the suit — retailers that carry these high dollar professional items could stand to bring in a new crop of newer, younger customers if they choose to work with BNPL platforms. This consumer is trying to look the part of someone who’s on their way for success and they’re putting in the work: they’re 37% more likely to be on LinkedIn than the average American consumer.

Source: Resonate Ignite Platform™, August 2021

Insight Three: 55% Say They’re Just Getting By Financially

This group probably wouldn’t use BNPL options if they didn’t have to, but they’re just getting by. They’re trying to find their footing in the world and BNPL is helping them bridge that gap.

Insight Four: 47% Have Two to Three Credit Cards

However, they may be using BNPL because they already have maxed out their credit cards. 40% carry a balance month-to-month and they are 2X more likely than the average consumer to only make minimum payments. BNPL platforms should explore the protections that can exist to protect their users, themselves, and retailers.

These BNPL consumers are more likely than the average consumer to use Wells Fargo as their primary credit card. One company you won’t notice on this list: Chase. As one of the biggest credit card issuers in the country, Chase should have this audience on their radar as an opportunity.

Meanwhile, these BNPL consumers are also more likely to have Synchrony Financial cards as their primary credit card. Never heard of Synchrony Financial before? That’s because they’re one of the biggest backers of store credit cards. Retailers rely on store credit cards for loyalty. If consumers are tempted to leave their store credit card for an interest-free BNPL platform with a different retailer, these retailers and Synchrony Financial could suffer.

Insight Five: Find Them on TikTok

We’ve explored Gen Z’s relationship with TikTok before so we know this is a critical channel to reach them. Whether you’re a retailer now offering BNPL as an option or a BNPL platform looking to reach potential users, TikTok is your space to advertise directly to your target audience.

Looking for more ways to get to know buy now, pay later customers? Or wondering what data Resonate can pull on your target audience? Request a demo today for a behind-the-scenes look at our all-in-one, easy-to-use platform.